jetcityimage

With inflation on the rise, many investors may wish to seek the safety of Treasury inflation-protected securities by investing in TIPS-focused funds such as the iShares TIPS Bond ETF (NYSEARCH: COUNCIL), the Schwab US TIPS ETF (SCHP), or the PIMCO Broad US TIPS Index ETF (TYPZ).

While individual TIPS may be protected from inflation with adjustments to their principal and coupons, investors are reminded that a TIPS fund still suffers from duration risk, which has led to losses to date. One possible solution may be to keep the fund focused on TIPS like the TIP as a pair trade against a medium-term treasury bond fund like the IEF.

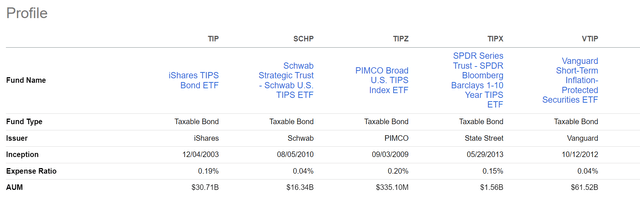

Abstract of funds

While this article focuses primarily on the iShares TIPS Bond ETF, the insights are applicable to other TIPS-focused funds such as SCHP and TIPZ. The TIP ETF is a fund that aims to track the returns of an index of US Treasury inflation-protected bonds. It has $30 billion in AUM.

Strategy

TIPS-focused ETF funds provide convenient vehicles for investing in US TIPS, government bonds whose face value rises with inflation.

Treasury Inflation-Protected Securities (“TIPS”) are well-known bonds issued by the US Treasury Department that provide protection against inflation. The principal of a TIPS increases with inflation as measured by the Consumer Price Index (“CPI”) and decreases with deflation. When a TIPS expires, investors are paid the greater of the adjusted principal or the original principal.

TIPS pay semi-annual fixed-rate interest calculated on adjusted principal, so interest payments also increase with inflation.

portfolio holdings

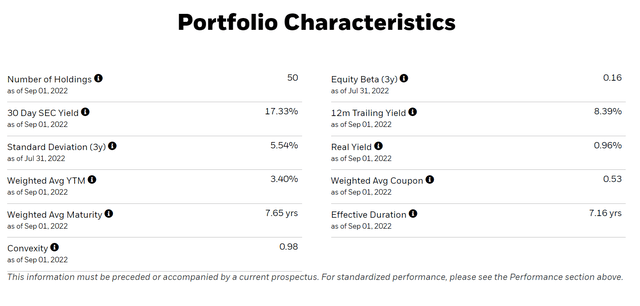

99.75% of the TIP ETF’s portfolio holdings are invested in US TIPS, with the remainder invested in cash for cash flow management purposes. The fund has more than 50 different TIPS issues, with a weighted average maturity of 7.65 years and an effective duration of 7.16 years (Figure 1).

Figure 1 – Overview of the TIP (ishares.com)

returns

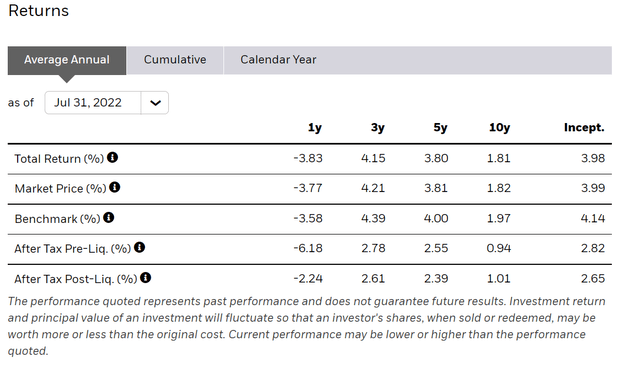

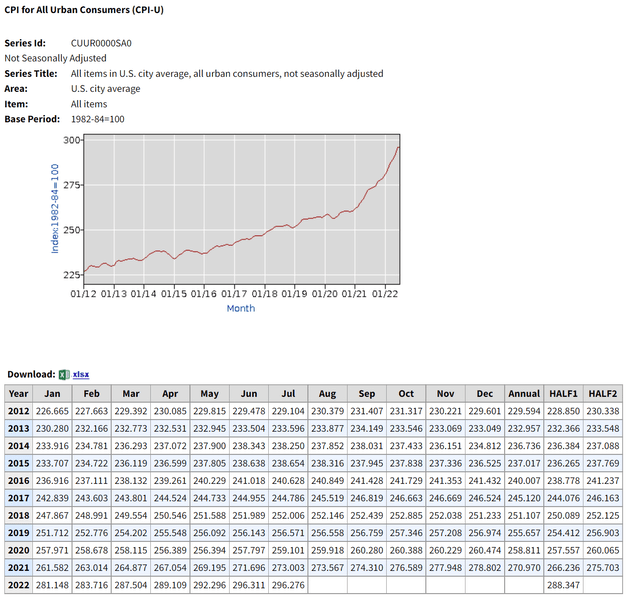

TIP has generated 5-year average returns of 3.8% and 10-year average returns of 1.8% (Figure 2). Note that the CPI index has been compounded at 3.8% for the last 5 years and 2.5% for the last 10 years (Figure 3), so the TIP ETF has underperformed inflation long-term.

Figure 2 – TIP average annual returns (ishares.com)

Figure 3 – CPI Index Values (data.bls.gov)

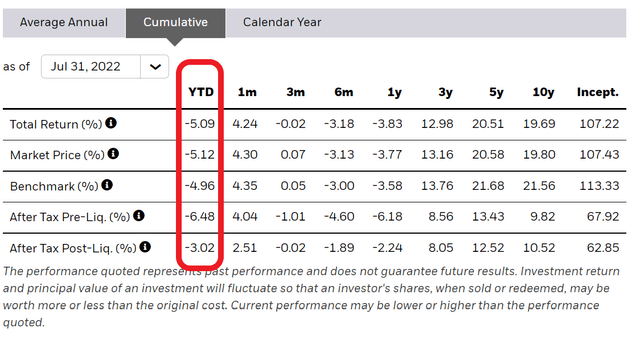

YTD, the TIP ETF is down 5.1% (Figure 4).

Figure 4 – TIP YTD Returns (ishares.com)

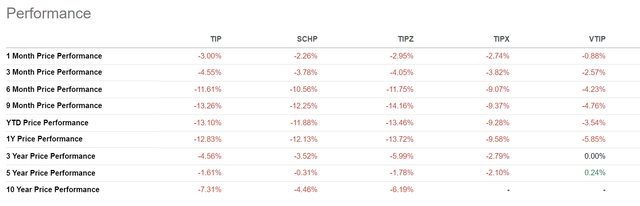

Compared to different TIPS-focused ETFs, the TIP ETF performs similarly to peers such as SCHP and TIPZ (Figure 5). All TIPS-focused funds have declined YTD based on price and NAV.

Figure 5 – TIP vs. peers (Looking for alpha)

Distribution and Yield

Where TIPS-focused ETF funds really shine is in their distribution performance. Remember that TIPS pay a coupon that is adjusted for inflation. This means that the investment income earned by these funds is also adjusted for inflation and paid out by the funds to investors.

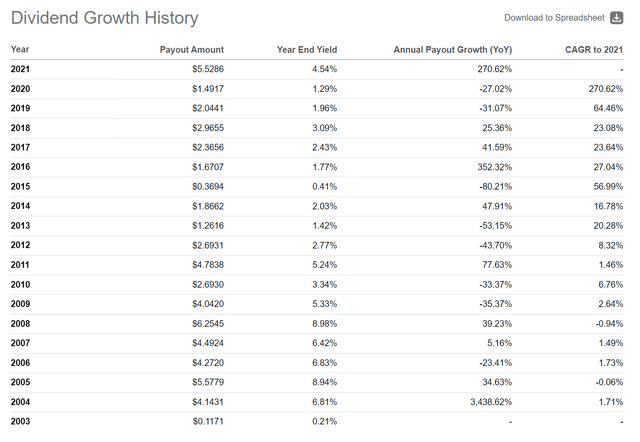

From Seeking Alpha, we see that the TIP ETF distribution has actually increased in 2021 and 2022 YTD (Figures 6 and 7). The 2021 distribution jumped 270% year over year to $5.53 per share and so far in 2022, TIP has paid or declared $6.93 per share.

Figure 6 – TIP distribution history (Looking for alpha)

Figure 7 – TIP YTD Distribution (Looking for alpha)

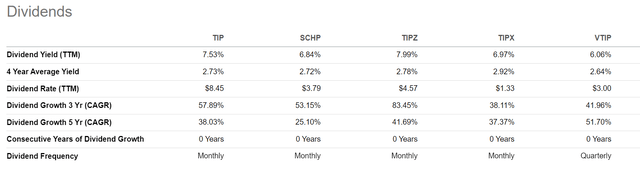

Comparing between the TIP ETF and its peers, we see that distribution returns are also very similar. TIP has an LTM dividend yield of 7.5%, while SCHP is 6.8% and TIPZ is 8.0%.

Figure 8 – TIP performance vs. peers (Looking for alpha)

Rate

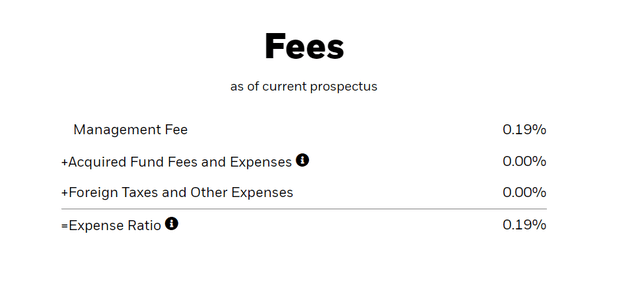

In absolute terms, TIP is a fairly low-cost fund, with an expense ratio of just 0.19% (Figure 9).

Figure 9 – Proportion of expenses of tips (ishares.com)

However, compared to pairs such as SCHP and VTIP, the TIP ETF is relatively high cost (Figure 10).

Figure 10 – TIP vs Peer Rates (Looking for alpha)

Inflation protection may not apply to a fund

Astute readers will note from Figure 4 above that the TIP ETF is down 5.1% YTD through July 31, despite paying $4.34 per share in distribution (3.4% of 2021 NAV YE of $128.95). This compares poorly to July’s headline CPI inflation rate of 8.5%. What an ‘Inflation-Protected’ Stock Fund Looks Like down YTD when inflation spikes? What’s going on?

What happens is that while the individual TIPS have their capital and coupons adjusted to the IPC index, as briefcase, the fund is subject to interest rate risk like other bond funds. Notice from Figure 1, the TIP ETF portfolio has an effective duration of 7.16 years. This means that for a 1% increase in interest rates, the portfolio is expected to lose 7.16% in value. As interest rates rose this year in response to runaway inflation, the TIP ETF’s NAV declined. At the end of July, TIP’s NAV has decreased by 8.5% to $118.03, which has more than offset paid distribution.

A similar analysis can be done on the other TIPS-focused funds. For example, SCHP has declined 7.9% YTD on a NAV basis while paying $1.88 per share in distribution (3.0% return on 2021 YE NAV of $62.83), for a total return of – 4.9% YTD.

Pairs trading may be the answer

Is there a solution to the duration problem? The short answer is yes, there is potentially another way to benefit from TIPS inflation protection without the duration risk. However, readers should understand that the following discussion is for educational purposes only and may not be achievable in practice (i.e. securities may not be available to borrow or fees to borrow securities exceed the benefit).

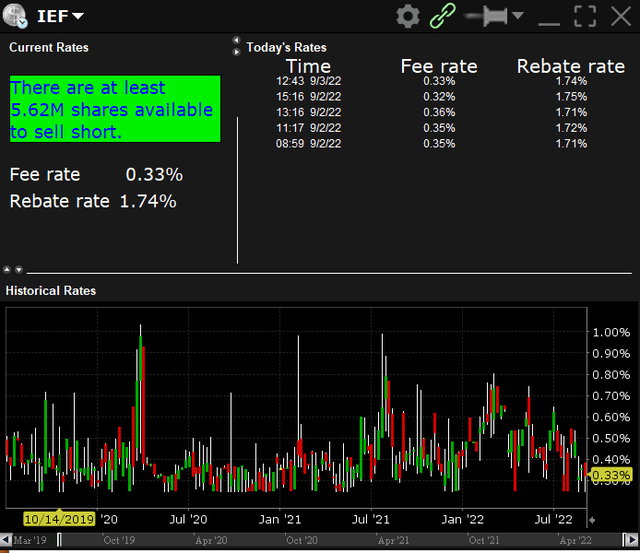

One possible solution to the above problem is to keep the fund focused on TIPS such as the TIP ETF, hedged with a short position in the iShares 7 – 10 Year Treasury Bond ETF (IEF) or a similar ETF. The IEF ETF is a $23 billion AUM ETF with an effective duration of 7.9 years. Assuming the two positions are theoretically hedged (i.e. holding $100 TIP and $100 short IEF), trading the pair could have generated a positive return of 3% as of July 31, before any fees (Figure 11).

Figure 11 – Trading of theoretical pairs between TIP and IEF (Author created with price chart from stockcharts.com)

Similarly, a pair between SCHP and IEF could have generated 3.2% (Figure 12). While a pair between TIPZ and IEF could have generated 2.4%.

Figure 12 – Theoretical torque between SCHP and IEF (Author created with stockcharts.com price chart form)

Of course, pairs trading assumes that investors are comfortable with short positions and can find a loan in the IEF ETF. The IEF is currently available to short on Interactive Brokers at an annualized fee rate of 0.33%, but note that the lending rate has been as low as 1% historically (Figure 13).

Figure 13 – Current loan rate in IEF (Interactive Brokers)

conclusion

With inflation on the rise, investors may want to seek the safety of inflation-protected Treasury securities through TIPS-focused ETFs like the TIP ETF. While individual TIPS may be protected from inflation with adjustments to their principal and coupons in the CPI Index, investors are reminded that a TIPS fund such as the TIP ETF still suffers from duration risk, which has led to a 5.1% year-to-date loss for the TIP. ETF and 4.9% year-to-date loss for the SCHP ETF. One possible solution may be to keep the TIPS-focused ETF as a pair trade against a medium-term Treasury ETF like the IEF.

Source: news.google.com