eduardoolivo

There is no telling how much further the rally in gold prices has to go, and speculative demand may well see the metal reach its all-time highs of $2,075. However, for those of us with a fundamental mind, now It doesn’t seem like a good time to invest. The rally is completely unrelated to its historical drivers. Real bond yields would have to drop significantly to justify current gold prices. In which case, it is likely that investors would be better off investing in TIPS.

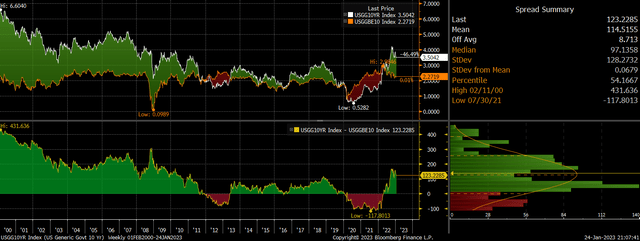

As I noted earlier this month, short-term movements in gold prices are closely tied to real bond yields, specifically the long-term US TIPS (Treasury Inflation Protected Securities) yield. When real bond yields are high and rising, the opportunity cost of holding gold, which pays no interest, increases. 10-Year Real Bond Yields Hold near their cycle highs, at 1.2% currently, reflecting expected inflation of 2.3% and the yield of 3.5% on the regular US Treasury.

10-Year UST Yields, Inflation Expectations, and 10-Year TIPS Yields (Bloomberg)

As the chart below shows, the last time real returns were at these levels was in 2011, when the price of gold was trading below $1,400. At this metric, real returns would have to fall back below -1.5% to justify current gold prices.

US 10-Year TIPS Yield vs. Gold (Bloomberg)

Even when we compare gold prices to the total return yield of 10-year TIPS, adding the impact of inflation, gold prices are still deeply overvalued. The current fair value is around $1,700.

Gold vs. US Inflation-Linked Bond Total Return Index (Bloomberg)

The only time we have seen gold rise against high real bond yields was during the 2003-2007 period, which saw widespread appreciation of commodities in response to booming Chinese growth and growing global liquidity. Today, global demand for commodities appears to be easing, as evidenced by the drop in the Bloomberg Commodity Complex, while the US money supply wobbles into a contraction for the first time on record. These are not the conditions under which we should expect a sustained rally in gold.

TIPS offer a better risk-reward perspective

We will likely need real bond yields to fall sharply to justify current gold prices. Over time, I expect this to happen, and I wouldn’t be surprised to see 10-year real yields go back below zero by the end of the year (see ‘TIP: The Great Monetary Reversal Has Started’). However, it is likely that investors would be better off investing in TIPS. Depending on maturity, TIPS yield around 1-1.5% and will generate income in line with inflation, almost guaranteeing positive real returns. This is not something that can be said for gold, which is also much more volatile than TIPS.

Source: news.google.com