TIPS and Treasury Bills

Note: This article was intended to be a follow-up to Tuesday’s “TIPS vs. Balanced Funds for Income: The Story” by providing some future perspective. However, in preparing that material, I realized that I could not do the subject justice without discussing a peculiar aspect of TIPS: its relative performance is better when inflation is low. under.

Treasury bills are the main investment rival to long-term inflation-protected Treasury securities. Conventional Treasury bonds do not follow market movements and other fixed income securities are not backed by the United States government. However, like TIPS, Treasury bills have both attributes.

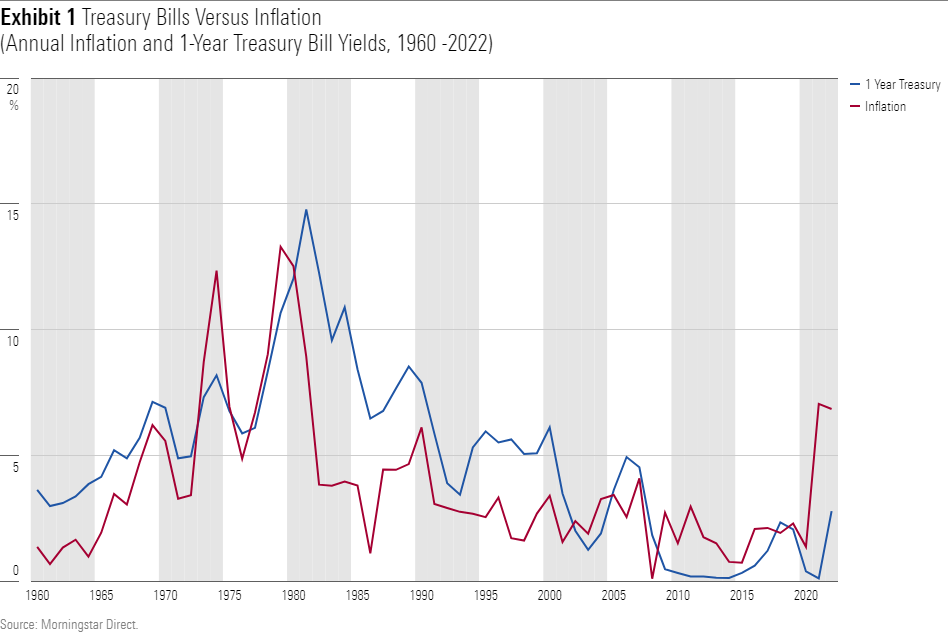

Officially, of course, Treasury bills differ from TIPS in that they are not specifically designed to track the rate of inflation. Unofficially, however, they have done just that. In 1959, the Treasury Department began regularly issuing one-year Treasury bills. Since then, the returns on those investments have consistently tracked the consumer price index. Where inflation has gone, so have one-year Treasury bills.

During that period, bills yielded an average of 4.85%, while inflation was 3.78%. Its real return was therefore 1.03%. (Or 1.07%, if you prefer the near-exact shortcut.) That’s close to the current real yield on 30-year TIPS, which is 1.46%. Therefore, the choice of investors seeking safe and inflation-protected income could be considered to consist of two investments with similar expected returns but different characteristics. One is stable with an implicit inflation adjustment, while the other is volatile, with an explicit insurance. (Another way of putting the matter, according to Bill Bernstein, is that short-term Treasuries are risky in the long term and riskless in the short term, while long TIPS are the opposite.)

The effect of inflation rates

Although true, that analysis is incomplete. Missing is the fact that the returns on those two investments are not comparable. They certainly seem to be. Treasury bills have been shown to have earned 1% more than the rate of inflation, while long TIPS are guaranteed by the government to deliver a bit more. But in practice, those figures convey very different things.

To explain this, let’s consider two hypothetical investors. One places $10,000 in newly issued one-year Treasury bills, spending the proceeds when those bills mature (because Treasury bills pay their proceeds through appreciation rather than coupons, the spread between their purchase price and its redemption value represents its yield). Then reinvest 10,000 in a new batch of one-year bills. The other investor puts $10,000 into 30-year TIPS, spends that year’s actual yield, and retains.

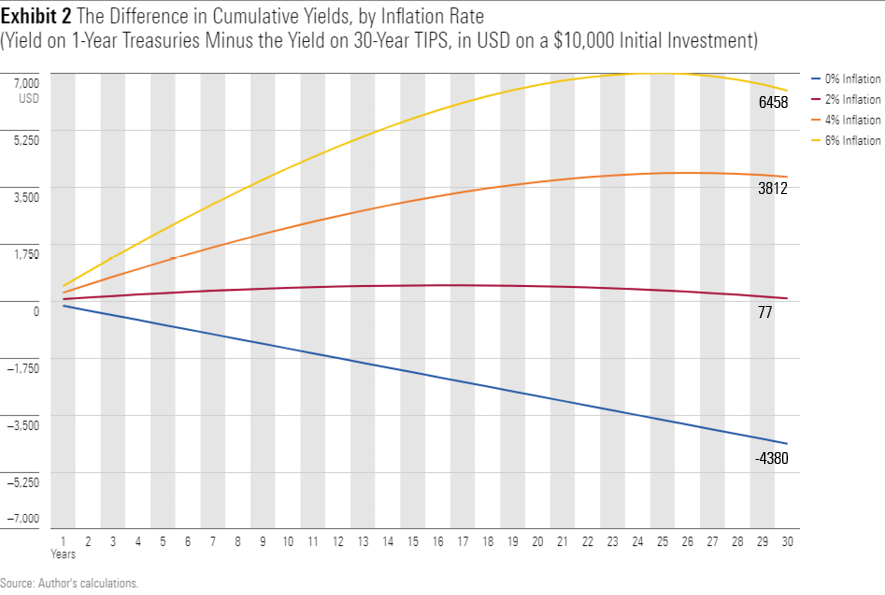

For this exercise, I will treat one-year Treasury bills conservatively. Rather than assume that they will provide a real 1% return, based on their track record, I will stipulate that they will provide no real return. Your aggregate return will exactly match the rate of inflation. Given that condition, surely 30-year TIPS will provide the best return.

Not so fast. It is true that TIPS will easily win the contest if the inflation rate is zero. If that were to happen, under the terms of this exercise, a strategy of investing in one-year T-bills would pay nothing for the next 30 years. (If that seems unrealistic, consider how low one-year rates have been in recent years, even when inflation was modestly positive.) Meanwhile, 30-year TIPS would pay a constant $146 on that $10,000 investment. That number would not increase, given that inflation is non-existent, but it does not need to increase for TIPS to outperform one-year Treasuries.

So far so good. The investment with the higher real return also pays a higher real return. However, the result is quite different if inflation increases. Let’s say inflation averages 6%. In that case, the one-year Treasuries would initially pay $600, with the 30-year TIPS once again at $146. Eventually, the yield on TIPS will catch up because each year inflation will increase the principal value of that value, and therefore the cash payments it distributes, based on its real yield of 1.46%, while the one-year Treasury will stall at $600. However, one-year Treasury bonds have a very big advantage!

Too big, in fact, to be captured in the next 30 years. The chart below shows the cumulative income gap between holding 1-year T-bills with zero real yield and holding 30-year TIPS with 1.46% real yield. A positive number indicates that one-year Treasuries have paid more cash thus far, while a negative number shows an advantage for 30-year TIPS.

That result is doubly strange. First, the relative results of two inflation-protected investments vary greatly depending on the level of inflation. Who would have guessed that? I do not. Furthermore, the investment with the lowest real return offers a significantly higher return over a 30-year period in two of the four cases. More and more curious.

Considering the present value

The above calculation, it must be confessed, ignores two critical factors. One is the time value of money. The income that is paid today is worth more than the income that comes tomorrow. For inflation rates above 1.46%, that math favors Treasury bills, which have the highest initial yield. The other element is principal repayment, which gives TIPS an advantage. Unless the inflation rate is zero, TIPS will be worth more than $10,000 when redeemed 30 years from now.

As a result, the last item is more important than the first. Evaluating the strategies for their present value shows that TIPS is the superior option regardless of the rate of inflation. (For example, 30 years into the strategy, a 6% annual inflation rate will have eroded 83% of the Treasury’s one-year purchasing power.) This result makes sense, since the exercise gave the TIPS strategy a considerable advantage in real terms. produce. Normalcy has been restored.

Resume

In a sense, 30-year TIPS is the most predictable investment. Over three full decades, long TIPS generate real cash flows that can be known in advance. Consequently, if they choose, TIPS owners can use their securities to build an investment ladder that provides a guarantee of payment that cannot otherwise be achieved.

However, from another perspective, long TIPS have strange and unpredictable properties. Not only do their market prices sometimes defy expectations, as was the case with last year’s crash, but when they compete for yield against their closest competitors, short conventional Treasuries, they are affected by the prevailing rate of inflation. , though not in the direction one would expect.

John Rekenthaler ([email protected]) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s investment research department. John is quick to point out that while Morningstar generally agrees with the views of the Rekenthaler Report, his views are his own.

Source: news.google.com